")

The buyer’s lens on revenue:

At Self Storage Advisory Australia, a key component of evaluating an asset’s listing price is assessing current performance relative to its potential performance. This helps us identify where buyers are likely to recognise value-add opportunities. When assessing a facility, revenue metrics are not only a reflection of current trading performance; they are a key indicator of income quality, pricing discipline and potential upside. In our article, Maximising Self Storage Article, we outline a framework in which Gross Potential Rate (GPR) represents the monthly rate advertised to a new customer for a vacant unit, Actual Occupied Unit Rate (AOUR) reflects the rate being paid by in-place customers, and Effective Occupied Unit Rate (EOUR) captures the net rate realised after discounts and incentives are applied.

Considered together, these measures provide a structured lens through which to evaluate both current income and future revenue potential. GPR indicates where management has positioned advertised pricing relative to the market. AOUR provides insight into the extent to which in-place customers have been brought toward that level. EOUR reveals whether discounting or promotional activity is materially affecting realised income. The relationship between these metrics can be highly informative. A material spread between GPR and AOUR may indicate embedded rental reversion, while a divergence between AOUR and EOUR may point to income leakage through discounts or concessions.

Importantly, these measures can also assist in identifying assets where performance is being constrained not necessarily by market competition, but by poor operational execution.

This is particularly relevant in regional markets characterised by limited competing supply, where a facility may already occupy a leading position within its catchment yet remain under-optimised from a revenue management perspective. From our standpoint, this distinction is critical, as incremental improvements in revenue can have a meaningful impact on capital value when income is capitalised.

At the same time, these metrics have limitations. They do not explain whether rental reviews are undertaken systematically, whether pricing is adjusted in response to changes in occupancy or availability, whether discounting is strategic or habitual, or whether occupancy leakage is occurring through poor enquiry conversion or weak operating controls. In that respect, the framework identifies the location of the revenue gap, but not necessarily its cause or the practical pathway to remediation.

The gap between potential and reality:

In our experience, many owner-managed facilities underperform not because of the quality of the asset, but because of operational inefficiencies that negatively impact revenue. Manual pricing practices, inconsistent in-place rent increases, prolonged discounting and limited visibility over occupancy and conversion are common examples. These issues are not inherent to the underlying real estate.

This distinction is fundamental in an acquisition context. A structurally challenged asset may require significant capital expenditure, repositioning or a material shift in market dynamics to improve performance. By contrast, a well-located facility in an undersupplied market may already possess the demand drivers, physical utility and competitive positioning required to outperform, yet still fall short of its income potential because pricing and revenue management practices lack discipline.

We observed this dynamic directly in a recent sale we transacted on. Following the acquisition of an owner-managed asset in a regional undersupplied market, the new ownership introduced a professional third-party manager and, over the first four months, achieved a 7.4% increase in occupancy, implemented 6% near-term in-place rent increases through a formal rate management schedule, increased new customer rates by 6–10%, and delivered a 7.6% uplift in RevPAM (Revenue Per Available Metre). Notably, this was already the premier facility in its market. The improved performance was not attributable to a change in marketing, product mix or competitive position; it was the result of a more disciplined approach to revenue management.

For us, this reinforces an important principle: underperformance is not always a negative indicator, and in many instances, it represents an opportunity.

Where the asset fundamentals are sound, the gap between potential and realised performance can often be narrowed through better systems, stronger reporting and more consistent pricing execution.

This is where technology becomes an essential operating tool, enabling managers to identify missed revenue, implement structured rate management, reduce discount leakage and improve overall operating efficiency.

The tech stack as a valuation multiplier:

Location has always mattered in real estate and self storage. In today’s market, the operations that are pulling ahead aren’t just well-located, they’re well-run. Increasingly, the differentiator comes down to technology.

This isn’t about novelty. It’s about what a connected, automated operation does to the numbers that actually drive valuation. When a facility moves from manual processes to automated move-ins, it removes friction at the point of conversion.

Frictionless conversion means higher occupancy, faster lease-up, and fewer staff hours absorbed by administration.

When dynamic pricing replaces static rate cards, revenue adjusts in response to real demand rather than trailing behind it. When managers have real-time visibility across a portfolio, not a spreadsheet updated at the end of the day, decisions get made faster and operational leakage gets caught earlier.

Each of these improvements has a downstream effect on Net Operating Income (NOI). And because self storage valuations are heavily influenced by income, anything that sustainably lifts NOI lifts the asset’s worth.

For buyers, this creates a useful filter. A facility running on legacy systems or manual workflows isn’t necessarily a poor asset; it may simply be an underperforming one. The technology gap is often the gap between what it earns today and what it could earn under competent operational management. That’s not a risk; in the right hands, it’s the opportunity.

For operators preparing to exit, the same logic applies in reverse. A business that has already made the shift is one that a buyer can step into with confidence. It signals operational maturity, reduces perceived transition risk, and supports a stronger valuation conversation from the outset.

In other words, the technology stack isn’t a cost centre. It’s a statement about the quality of the income the business produces.

What good looks like:

If the technology stack is the engine, the Facility Management Software (FMS) is the foundation it runs on. Everything else (pricing tools, tenant apps, remote access, reporting dashboards) depends on the FMS being the right fit for the business.

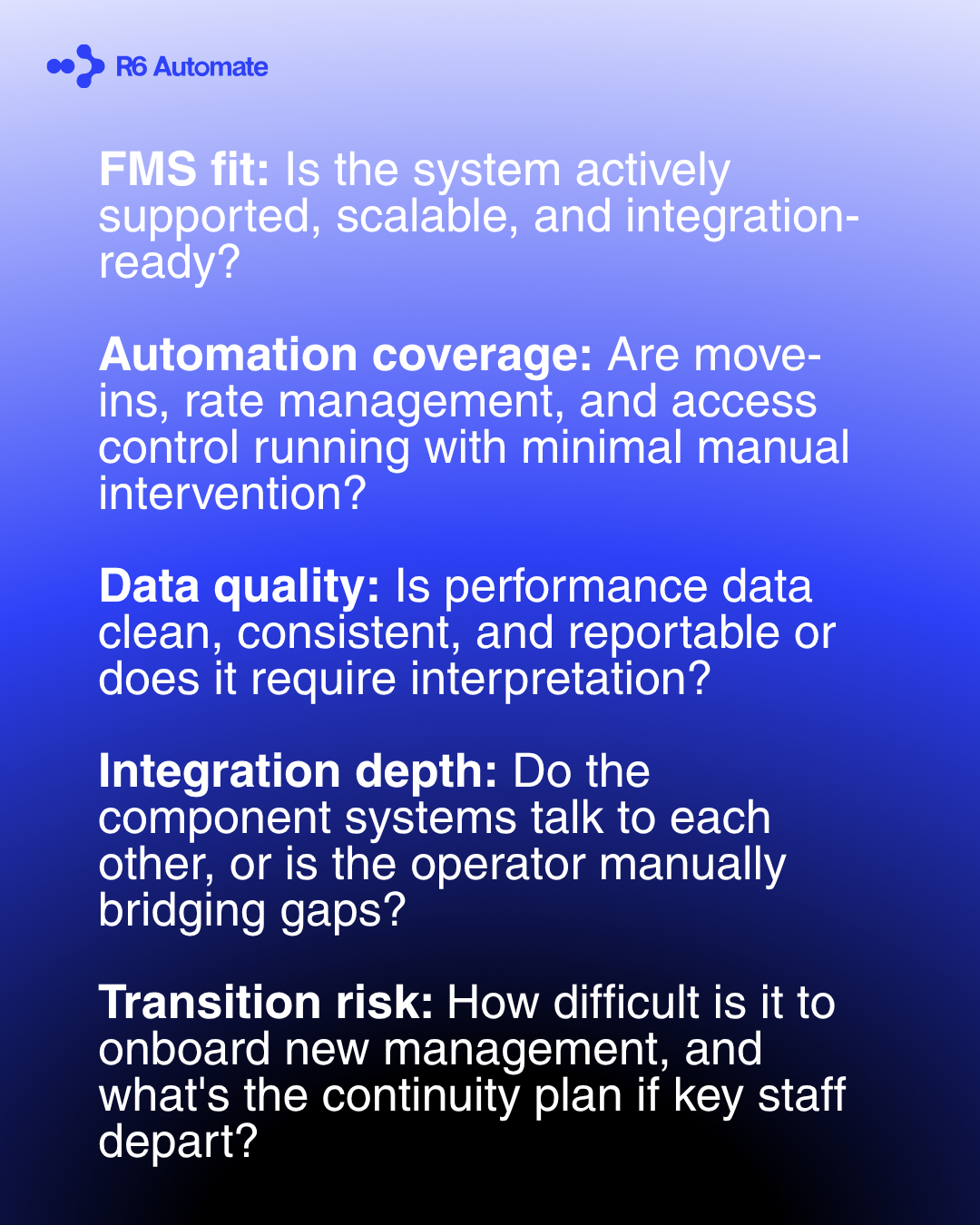

For buyers assessing an acquisition, the FMS warrants closer scrutiny than it typically receives. The questions worth asking go beyond whether the software is current. Is it widely supported? Does it integrate with the tools that drive revenue and efficiency (online booking, dynamic pricing and access control)? Can it scale across multiple sites without creating operational silos? Finally, does it produce reporting you can actually rely on? Working with data that’s incomplete, inconsistent, or difficult to extract makes it genuinely hard to know what performance is being achieved, which complicates due diligence for buyers and weakens the story for sellers.

For operators thinking about exit, the FMS layer is also where pre-sale preparation pays dividends. A well-configured system with clean data, automated workflows, and proven integrations tells a coherent operational story. It gives a buyer visibility into performance, reduces the due diligence burden, and removes one of the more common points of uncertainty in any acquisition conversation.

Platforms like SiteLink, when paired with complementary tools such as automated move-in and booking via RapidStor, tenant engagement through StorApp, and operational oversight through a consolidated dashboard like the R6 Automate Operations Centre, create an ecosystem where performance is measurable, repeatable, and transferable.

What matters most at the point of sale is that a buyer isn’t just acquiring a building and a customer list; they’re acquiring an operation. The cleaner and more connected the operation, the easier it is to price with confidence on both sides of the table.

The practical checklist for buyers isn’t long, but it is specific:

For operators, working through this list before going to market is time well spent. For buyers, it’s a framework for separating genuine operational strength from a facility that looks the part but carries hidden complexity underneath.

Buying or selling a self storage business requires seeing the full picture. The revenue metrics tell you where a facility stands; the operational infrastructure tells you where it could go. When both lenses are applied together, real estate expertise informing the asset assessment, and technology expertise informing the operational one, the gap between current and potential performance becomes something you can actually act on, not just observe. That’s the difference between a transaction and a value-creation opportunity.

For an opinion of value or value gap analysis, reach out to Self Storage Advisory Australia or email the team ([email protected]).

This article was written in collaboration with R6 Automate.

{kind=link}